Tomaso Aste

Head, Financial Computing & Analytics Group

Director, MSc Financial Risk Management

My research interests

Big Data Analytics The accessibility to large quantities of data combined with the great storage capabilities and cutting-edge computational tools makes possible to investigate complex systems, such as financial markets, in a new quantitative manner. I am developing tools to extract meaningful information from very large complex datasets.

Information

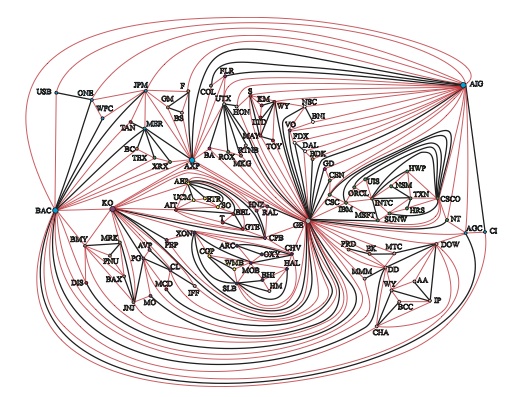

Filtering I investigate new ways to filter

information from complex data by constructing networks of

dependency and causality relations that provide information

about the collective behavior of the system, the heterogeneous

distribution of response to external or internal changes and

interrelation between the parts.

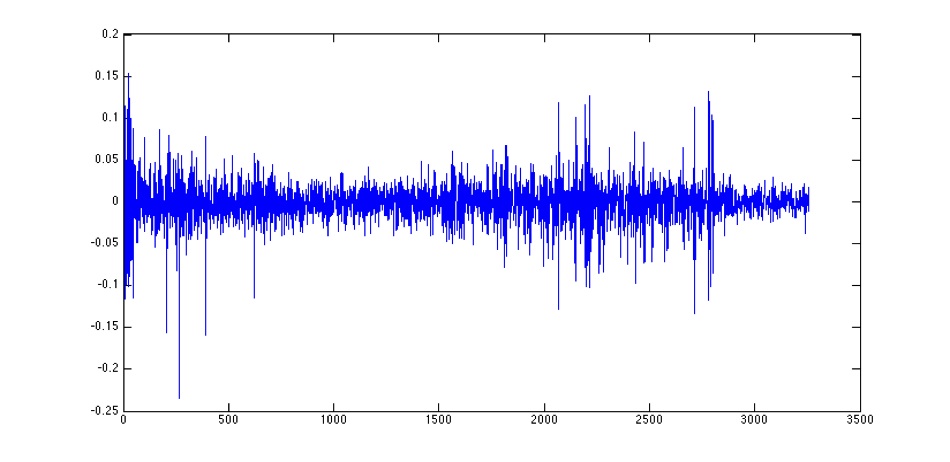

Scaling

and Muliscaling I investigate the complexity

of the evolution pattern of a variable in time extracting

scaling laws which can provide information on the stability of

the observed behavior and give insights on the future

evolution.

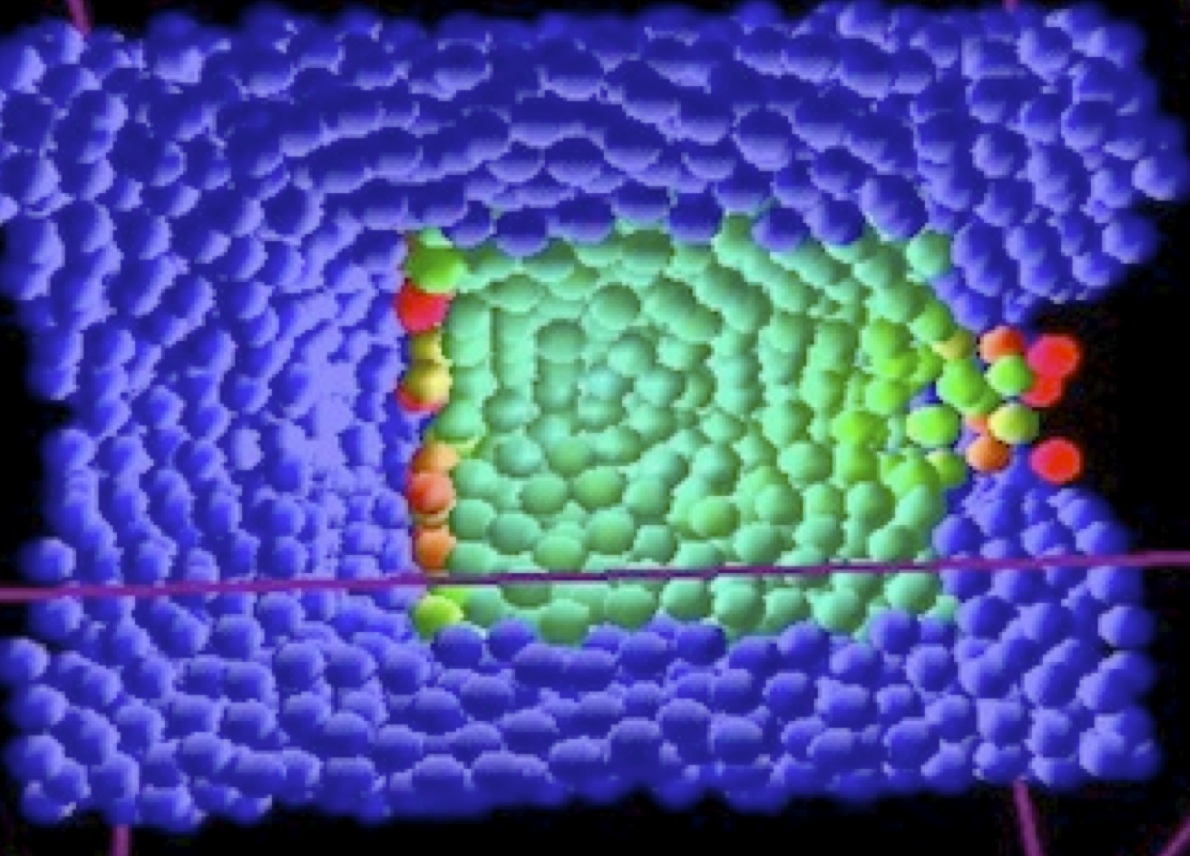

Complexity

I study how complexity can offer stability, robustness,

adaptation and spontaneous organization to complex systems.

Natural systems have long exploited complexity we are learning

from the biological world how to integrate complexity in the

design of new artificial systems.

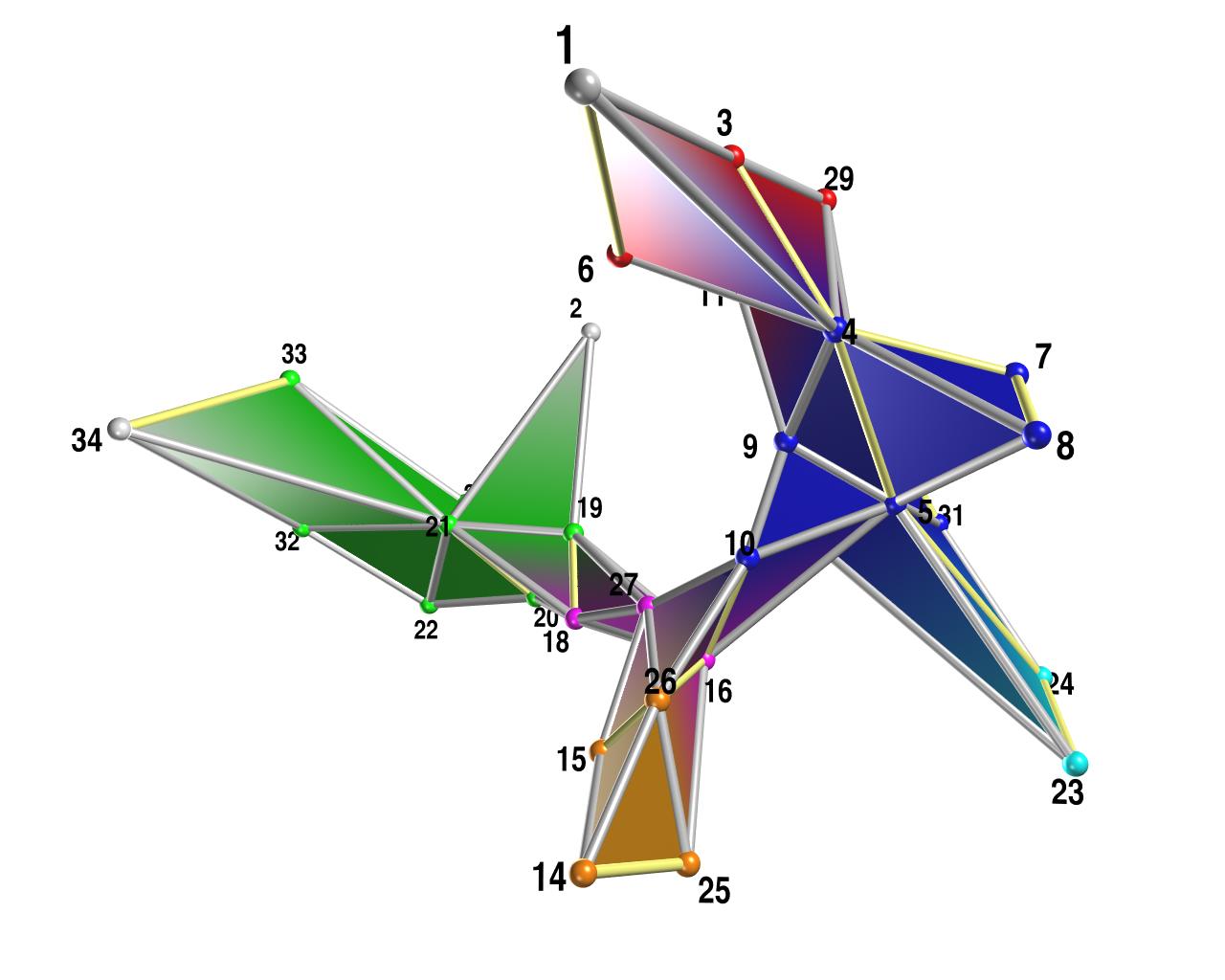

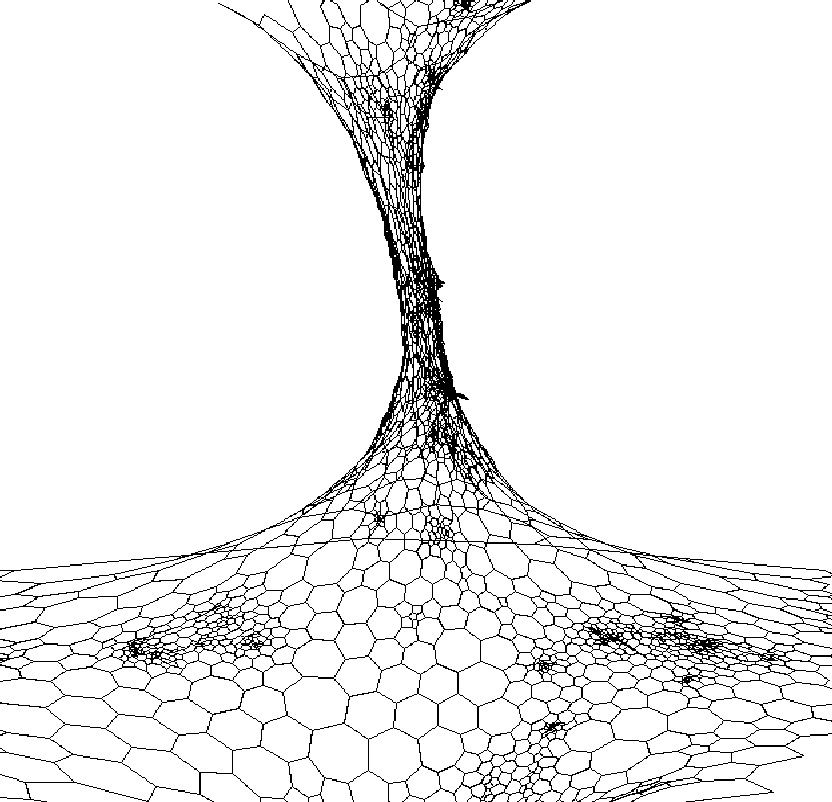

Networks

I explore novel methods to generate and characterize complex

networks by means of their embedding on hyperbolic surfaces.

This method provides a new perspective to network theory and

opens no ways to use networks for the investigation of complex

systems and financial markets.

Complex Matter I study how complexity manifest itself in the structure of real physical systems and why nature carefully selects only some realizations of randomness.